Alert: Beware of scammers impersonating Unity Bank staff. Never share login details or One Time Passwords with anyone.

This section provides help if you are stuck or can't find what you are looking for. It also has the answers to the most frequently asked questions.

What is the Boost to Buy Home Ownership Scheme?

The Boost to Buy Home Ownership Scheme provides an equity contribution to eligible applicants who are purchasing their first home in Queensland. By bridging the deposit gap between what can be borrowed and the price of a home, Boost to Buy is enabling earlier home ownership for eligible applicants.

How does Boost to Buy work?

Boost to Buy is a shared equity scheme. This means the Queensland Government makes a financial contribution towards the purchase of your home in exchange for ongoing equity in the property.

For successful Applicants, Boost to Buy will offer an equity contribution of up to 30% for new homes and up to 25% for existing homes. Participants will need to contribute a Minimum Deposit of 2% of the Purchase Price, as well as any Acquisition Costs, such as legal and conveyancing costs, transfer duty and mortgage registration fees. The remaining amount is to be secured through a home loan from an Approved Lender.

Boost to Buy Participants must repay the Queensland Government’s interest in the Property over time by refinancing, using accumulated savings, or upon sale of the Property. The Queensland Government will not charge interest on its equity contribution but will share in any capital gains or losses proportionate to its interest in the Property.

Who is eligible?

To be eligible the Applicant must meet all eligibility criteria:

You must not be receiving or have received assistance from one of more of the following:

Note: you may still apply for the Queensland Government First Home Owners Grant while participating in the Boost to Buy Home Ownership Scheme.

How many places are available?

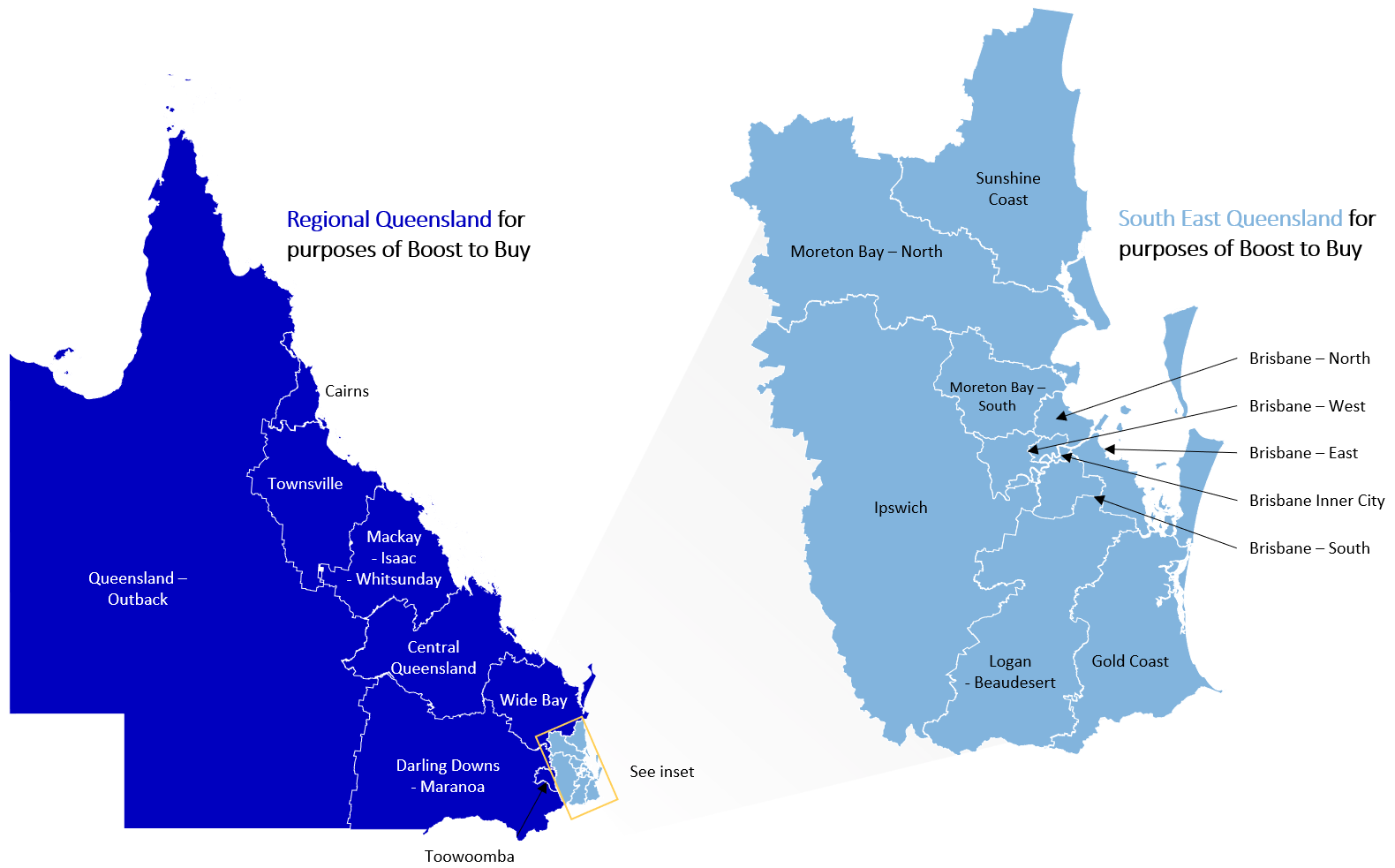

Can I buy anywhere in Queensland?

Half of the places in the Scheme are allocated to South East Queensland (SEQ) and the other half to regional areas.

The following Statistical Areas Level 4 (SA4s) defined under the Australian Statistical Geography Standard (ASGS) by the Australian Bureau of Statistics are included in SEQ vs regional for the purpose of the Scheme:

|

Regional Queensland:

|

South East Queensland:

|

You need to purchase an Eligible Property in the area for which you sought and received provisional approval. If you received a provisional approval for SEQ you must purchase within SEQ. If you received provisional approval for regional Queensland you must purchase within regional Queensland. You can use ABS Maps to identify what areas are covered by each SA4 area.

Are there any income restrictions?

Yes. The Scheme will be open to single applicants with a taxable income of up to $155,000 in the tax year ending June 2025. Single applicants with one or more dependents, or two adult applicants applying together, can have a combined taxable income up to $232,000 in the tax year ending June 2025.

What additional assistance is available for single applicants with one or more dependents?

Single applicants with dependents can access the Scheme based under the higher Income Thresholds (i.e. up to $232,000). Note: to qualify as a single applicant with dependent(s) for the purposes of the Scheme you must be a person with one (or more) dependent (children or adults) and without a Spouse or de facto partner. If you are separated but still married, you are not classified as single for the purposes of the Scheme.

Separated but still married parents would still be eligible to access the Scheme under the single Applicant Income Threshold (i.e. up to $155,000). However, if your Spouse has owned or currently owns Real Property, you will not be eligible for the Scheme as long as you are married.

I'm a New Zealand citizen living in Australia on a Special Category Visa (Subclass 444). Am I eligible?

No - you must be a permanent resident of Australia or an Australian citizen to participate in the Scheme. Please note that both protected and non-protected Special Category Visa (Subclass 444) are ineligible for the Scheme.

Can I enter into a contract of sale before obtaining provisional scheme approved?

No – unfortunately you will be unable to apply if you’ve already signed a contract of sale. Participants need to have a conditional lending approval in place with an Approved Lender and seek provisional Scheme approval before signing a contract.

How do I apply?

We suggest you check your eligibility using the eligibility tools at either www.treasury.qld.gov.au/boost-to-buy and via the Unity Bank chatbot. Note this is indicative only and your participation in the Scheme will be subject to Approved Lender and Scheme approval.

If you think you are eligible, you can use the Unity Chatbot to book a Boost to Buy appointment to request a loan assessment to determine your borrowing capacity and whether you can service a home loan. It is important to understand that while you may be eligible for the Scheme, you may not necessarily be eligible for a loan with an Approved Lender, in which case you will not be able to take part in the Scheme.

I have saved a 2% deposit, are there any other costs involved?

You will be required to pay all costs associated with purchasing your home (often referred to as acquisition costs) such as conveyancing, legal costs, building inspections and stamp duty. You may be eligible for stamp duty concessions and the Queensland Government First Home Owners Grant to assist with these costs, these will need to be applied for separately.

Can my deposit be more than 2%?

Yes. The required minimum deposit for applicants is 2% however your deposit can be more. Your deposit must be made up of genuine savings, as determined by the Approved Lender. The more you contribute to the deposit, the greater your equity interest in the property will be.

Do I have to take the full 25% (existing homes) / 30% (new homes) provided by the Queensland Government?

No – you do not need to access the full entitlement. However, at a minimum, the combined total of your deposit and the Queensland Government’s contribution must be at least 20% of the purchase price to meet an 80% loan to value ratio.

What is Shared Equity Interest, Shared Equity Amount and Shared Equity Money.

The Queensland Government will make a financial contribution (Shared Equity Money) towards the purchase of your Property in exchange for an equity interest in the Property, referred to as a Shared Equity Interest.

The monetary value of the Queensland Government’s Shared Equity Interest in your Property at any point in time will change subject to the value of your Property (i.e. the Queensland Government will share in any capital gains or losses proportionate to its interest in the property). The monetary value of the Queensland Government’s Shared Equity Interest at any point in time (other than at the time of initial acquisition of the property) is referred to as the Shared Equity Amount.

How is the Queensland Government’s Shared Equity Interest in my property calculated?

The Queensland Government will provide up to 25% of the purchase price for existing homes and 30% of the purchase price for new homes. The purchase price is derived from your contract of sale. However, the Shared Equity Interest will be calculated on the lower of the purchase price and the Approved Lender’s valuation of the property. In some instances this may mean the Queensland Government holds a greater than 25% share. For example:

Jason purchases a property for $900,000. The Approved Lender approves the home loan but the bank’s valuation is less than Jason’s purchase price ($870,000). The Queensland Government provides $232,000 in funding based on the purchase price and the bank is prepared to fund the balance.

Calculation example:

Shared Equity Interest = $232,000 / $870,000 = 26.67%

Based on the calculation above using the valuation amount, the Queensland Government’s Shared Equity Interest is grossed up to 25.86%. When Jason eventually pays the monetary value of the Queensland Government’s Shared Equity Interest back (either in full or gradually over time), the Shared Equity Amount will be based on the property’s prevailing market value — not the original purchase price.

The Queensland Government’s Shared Equity Interest (as calculated in the example above) is calculated on entry into the scheme and does not fluctuate throughout the course of your involvement in the Scheme unless you make voluntary repayments (except for in limited circumstances when non-compliance has occurred and a fee, which accrues on the Queensland Government’s Shared Equity Interest, is applicable). This is different to the Shared Equity Amount which is the monetary equivalent of the Shared Equity Interest, which is calculated at different points in time and will be based on the property’s prevailing market value.

Is interest charged on the Queensland Government’s Shared Equity Interest?

No interest is charged on the Queensland Government’s Shared Equity Interest, but as the value of your property changes, so too will the value of the Queensland Government’s Shared Equity Amount. Repayments of the Queensland Government’s Shared Equity Interest in your property, will reflect any increases or decreases in your property’s market value as determined by a valuation.

In limited circumstances when non-compliance has occurred, a fee which accrues on the Queensland Government’s Shared Equity Interest will be applicable.

Are there restrictions on where I can purchase a Property?

Yes – you need to purchase an Eligible Property in the area for which you sought and received provisional approval. If you received a provisional approval for SEQ you must purchase within SEQ. If you received provisional approval for regional Queensland you must purchase within regional Queensland.

Are all properties eligible?

All residential property in Queensland with a Purchase Price of $1 million or less and being purchased in your own name (i.e. not through a self-managed superannuation fund, company or trust structure) is considered to be Eligible Property for the purpose of the Scheme. Note that the eligible property must be in the area in which you sought and received provisional approval i.e. either within SEQ or regional Queensland.

Can I buy an established home?

Yes. If eligible, the Queensland Government would provide up to 25% of the purchase price.

Can I buy a new home?

Yes, provided a Certificate of Occupancy or Final Inspection Certificate has been issued at the date of signing a contract of sale. If eligible, the Queensland Government would provide up to 30% of the purchase price.

Can I buy a home off the plan?

No - properties not yet built are not eligible. A Certificate of Occupancy or Final Inspection Certificate must have been issued at the date of signing a contract of sale.

Do I have to live in the property?

Yes. You and all other participants attached to the application (if applicable) for the Scheme must live in the home as your principal place of residence as long as you are participating in the Scheme.

You may vacate your Property for 3 months, and if you need to vacate longer due to exceptional and unavoidable circumstances such as medical treatment for you or someone else, caring responsibilities based on medical grounds, education or an interstate or overseas posting in relation to your employment, you may seek consent to do so. You will not, at any time, be allowed to lease the entire Property to another person.

Can I still receive the Queensland Government First Home Owner Grant (FHOG) and Transfer (Stamp) Duty Concessions?

Applicants of the Scheme remain eligible for other Queensland Government concessions. If you are eligible for these concessions, you will be required to apply in the usual way.

Will I need to pay transfer (stamp) duty?

You will be required to pay the usual amount of transfer duty that applies at the time of settlement for the full cost of your property (unless you have been granted any Transfer Duty Concessions).

What happens if I want to sell my property?

You must notify your Approved Lender at least 30 days prior to engaging a Real Estate Agent. The Approved Lender will arrange for a valuation that will be used in the calculation of the Queensland Government’s Shared Equity Amount of the proceeds.

The Queensland Government’s Shared Equity Amount on sale will be calculated on the higher of the sale price and the Approved Lender Valuation. You will also be required to meet the full costs of selling your Property (e.g. real estate marketing and commission) including any upfront costs.

Example:

Ravi and Jess buy a property valued at $1 million through the Boost to Buy Home Ownership Scheme. They contribute a 2% deposit which is $20,000 and the Queensland Government makes a 25% contribution, which is $250,000.

Ravi and Jess continue to meet the Scheme eligibility requirements and do not make any voluntary repayments. After a few years, Ravi and Jess decide to sell their home. Before placing the property on the market they notify their bank who arranges for a Valuation. The Approved Lender Valuation comes back with a value of $1.13 million but Ravi and Jess sell the property for $1.1 million. The Queensland Government’s Shared Equity Amount payable would be based on the $1.13 million valuation.

Calculation of Shared Equity Amount:

Shared Equity Interest of 25% ×Higher of sale price and Panel Financier valuation of $1,130,000 = $282,500

The Queensland Government’s 25% Shared Equity Interest is now worth $282,500, which Ravi and Jess have to pay back from the proceeds of their sale. Their loan balance was $700,000 and real estate fees were $30,000, which was repaid with sales proceeds. After the real estate agent, the Approved Lender, and the Queensland Government have been repaid, Ravi and Jess receive $87,500 from the sales proceeds.

Is there a minimum period the property must be held for before it can be sold?

You are not permitted to sell your property within 2 years of the date of settlement without the prior written consent from the Queensland Government.

I was previously bankrupt. Am I eligible?

You can apply if you are not currently bankrupt (i.e. a discharged bankrupt), there is no impending bankruptcy, and you are not subject to a Deed of Assignment, Deed of Arrangement, Debt Agreement or Personal Insolvency Agreement. You will still be required to meet all other credit checks performed by the Approved Lenders.

I’ve been granted provisional approval. What happens next?

You will receive a letter detailing your indicative maximum purchase price (based on your deposit and in-principle loan approval amount) and the maximum financial contribution you may be eligible to receive from the Queensland Government, pending the satisfaction of certain conditions.

You will have six months to enter into a contract of sale for an Eligible Property.

What happens if I don’t enter a contract of sale within 6 months?

If you have not entered a contract of sale by the end of the 6 month period, you will no longer be eligible for the Scheme and will have to re-apply for the Scheme through the standard process.

What if I change my mind?

Before entering into a contract of sale, you can withdraw your application at any time by notifying the Queensland Government in writing.

What happens if the purchase price of my property exceeds the $1,000,000 price threshold?

The maximum Purchase Price for a Property purchased under the Scheme is $1 million. If you enter into a contract for more than $1 million, you will not have satisfied the Eligible Property Criteria for the Scheme and the Queensland Government will not provide the 25% or 30% equity contribution.

Acquisition Costs will be paid by the Participants and will not be included in the $1 million price threshold.

Are there any restrictions on the purchase methods when buying a property?

Your contract of sale must be a Contract for Sale and Purchase of Residential Real Estate provided by the Real Estate Institute of Queensland with a settlement period in line with standard terms (min 30 days). You must also include a 14-day finance clause to allow sufficient time for your home loan and the Queensland Government’s Shared Equity Money to be approved. It is recommended that you seek independent legal advice around the terms and conditions your contract should include.

You will not be able to purchase a Property at Auction, noting that auction purchases are unconditional in nature and final lending and final Scheme approval can only be granted once property eligibility has been assessed.

What happens after I sign a contract of sale?

You will need to pay the deposit at the time of entering into the contract of sale. You will also need to let your Approved Lender know you have entered into a contract of sale and intend to make a purchase so that preparations for settlement can be made. Within three business days of entering into the contract of sale, you will need to provide a copy of the signed contract of sale to your Approved Lender.

Following lender and Queensland Government Property eligibility assessments you will be sent a pre-populated Participation Agreement via DocuSign that will include your personal details, property details and outline the Shared Equity Money and Shared Equity Interest the Queensland Government will pay at settlement. You must sign this Participation Agreement within three business days of receiving. If you do not adhere to these time frames you risk that the Queensland Government’s equity contribution will not be made available in time for settlement.

You also need to ensure your Property is appropriately insured from the date you sign the contract.

What type of insurance do I need to take out on the property?

Your property must be insured against damage, destruction (including by fire, flood, storm, cyclone etc) and any other risk required by the Approved Lender to its full replacement value, or on a reinstatement basis.

For houses: A building/home insurance policy must be taken out with an authorised insurer and must note the interest held by the Security Trustee.

Strata titled: If your property is on strata title with an Owners Corporation, the policy will be under the Owners Corporation (not your name) and will not need to note the interest held by the Security Trustee. It is recommended that you check the extent of the coverage offered by the Owners Corporation insurance policy and acquire additional coverage if required.

You must provide a copy of either your building insurance or strata insurance certificate of currency when you provide your Approved Lender with the contract of sale.

Who is the Security Trustee?

The Security Trustee is an entity appointed to hold and manage the security interest (the mortgage) over your property on behalf of the Approved Lender (your bank) as the first ranking secured creditor and the Queensland Government as the second ranking secured creditor. Unity Bank is the Security Trustee.

Will I need a conveyancer/lawyer?

Yes. You must engage a lawyer or conveyancer for settlement of the property.

What is the process once I receive final approval?

You will receive a final approval letter detailing your Shared Equity Interest and Shared Equity Money, which is the financial contribution that will be provided by the Queensland Government at settlement.

Can the property be renovated?

Yes. You may renovate, extend or improve your Property as you see fit and at your own cost, however the Queensland Government will retain its Shared Equity Interest in your Property until you repay it in full. Therefore, where the Queensland Government still has a Shared Equity Interest in your Property that you have made improvements to, the Queensland Government will share in any upside/capital gains generated from your renovations.

Participants are encouraged to consider repayment of the Queensland Government’s Shared Equity Interest before undertaking renovations, extensions and improvements.

I would like to repay some of the Queensland Government’s Shared Equity Interest. How is the value of the Shared Equity Interest determined at that time?

If you intend to use savings to repay you will need to provide the Queensland Government with a valuation that they can rely on from a valuer registered with the Valuer Registration Board of Queensland.

If you intend to increase your loan to repay some or all the Queensland Government’s Shared Equity Interest, your Approved Lender will provide the Queensland Government a Valuation. A Valuation must have occurred within 12 months of the date on which that calculation, assessment or evaluation is made. The Valuation will be used to calculate the Shared Equity Amount (i.e. the monetary value of the Shared Equity Interest) in the property at or around the time of payment.

When am I required to repay the Queensland Government’s Shared Equity Interest in full?

You will be required to repay the Shared Equity Amount in full either when:

You will also be required to repay the Queensland Government’s Shared Equity Interest early if you breach the terms and conditions of the Participation Agreement. In these circumstances, you will be issued an Early Payment Notice requiring you to repay the Shared Equity Interest in full.

How do I exit the Boost to Buy Scheme Home Ownership Scheme?

You are required to remain in the Scheme and hold the property as your principal place of residence for at least 2 years from the date of settlement, unless exceptional circumstances occur, and the Queensland Government consents to this in writing.

After this time, you can exit the Scheme by either selling your property or repaying the Queensland Government’s Shared Equity Amount (being the monetary value of the Shared Equity Interest) in full. The latter can be done by refinancing your home loan (pending approval from your Approved Lender), or through voluntary payments using savings. Valuations will need to be arranged in order to determine the value of the Government’s Shared Equity Interest.

Can I make a voluntary payment and what is the process?

Yes. Your payment will need to reduce the Shared Equity Interest by at least 5 percentage points (e.g. from 25% Shared Equity Interest to 20% Shared Equity Interest).

To determine the market value of your property, if you are planning to use savings to make a voluntary payment, you will need to provide a valuation from a valuer registered with the Valuer Registration Board of Queensland. Alternatively, you can approach your Approved Lender to see if you can increase your loan (i.e. refinance) to make a voluntary payment and your Approved Lender will provide a valuation. A Valuation must have occurred within 12 months of the date on which the calculation of Voluntary Payment is made.

Once the valuation is provided, the Queensland Government can advise you of how much the Shared Equity Interest will reduce based on your payment and you can choose whether you would like to proceed. When a voluntary payment has been made, the Queensland Government will send you a confirmation of the reduction in the Shared Equity Interest in your property.

Can I refinance my loan for other reasons (i.e. aside from making a repayment of Shared Equity)?

You can only increase your home loan with your approved lender to pay back the Queensland Government, or as otherwise permitted by the hardship provisions contained in the Consumer Credit Legislation.

Refinancing your home with a non-participating lender is not permitted and will require you to repay the Queensland Government’s Shared Equity Amount in full if you want to do so.

How are proceeds from the sale of my property treated?

The Queensland Government’s Shared Equity Interest in your property is secured through a second ranking security interest in the mortgage, second to your Approved Lender. If you sell your property, proceeds will be applied in the following order:

What happens if I lose my job or suffer financial hardship?

You should notify your Approved Lender immediately to discuss your options, noting that you are afforded certain protections under the National Credit Code.

What happens if a single applicant subsequently marries or enters into a de facto relationship?

Your ongoing eligibility for the Scheme will not change. However, if you and your new partner decide you want your new partner to also become a registered owner of the property, you will be re-assessed as joint applicants to see if you meet the eligibility criteria. Discuss with your Approved Lender the best way forward for your new partner to acquire an interest in your property.

What happens if my income increases over time and exceeds the income threshold?

If your income exceeds the annual income threshold by 25% in two consecutive financial years, you are obligated to notify the Queensland Government and you will be required to request a borrowing capacity assessment from your Approved Lender to find out how much you can increase your home loan to make a repayment the Government’s Shared Equity Interest (to the maximum extent possible). You will also receive a Valuation from your Approved Lender. The assessed increase in the home loan is the amount you have to repay the Queensland Government, as long as the increase represents more than 5 percentage points of the Shared Equity Interest. You can choose to repay via refinance of the home loan or via savings.

If your Approved Lender’s borrowing capacity assessment demonstrates that you are unable to make a repayment, or the repayment is less than 5 percentage points of the Shared Equity Interest, you are still eligible to participate in the Scheme. Your new audit intervals will be every three years. If you continue to exceed the Income Threshold at your next audit in three years’ time, the Queensland Government will ask you to seek another borrowing capacity assessment for repayment.

Can I vacate the property?

The property must be your principal place of residence. You cannot vacate the property for more than 3 months without Queensland Government approval. Generally, there must be exceptional and unavoidable circumstances to obtain approval for vacating (e.g. caring responsibilities on medical grounds). If the Queensland Government agrees, time limits may be imposed.

Can I rent out the property?

You may rent out a room to a housemate/flatmate (which is referred to as ‘licensing’) provided the property remains your principal place of residence (meaning you must continue to live in it) and you adhere to all other requirements.

If it is determined that your property is no longer your principal place of residence, you will need to move back in or pay back the Queensland Government’s Shared Equity Amount (being the monetary value of the Shared Equity Interest) in full. If you don’t comply, then a fee will accrue resulting in an increase in the Government’s Shared Equity Interest (resulting in a reduction in your equity interest). This fee will accrue every other year until you have repaid the Shared Equity Amount in full.

Can I purchase an investment property while in the Boost to Buy Scheme?

No. You cannot acquire an interest in any other real property asset while being a participant in the Boost to Buy Home Ownership Scheme.

If it is determined that you hold an interest in any other real property asset in Australia, you will need to pay back the Queensland Government’s Shared Equity Amount (being the monetary value of the Shared Equity Interest) in full. If you don’t comply, then a fee will accrue resulting in an increase in the Government’s Shared Equity Interest (resulting in a reduction in your equity interest). This fee will accrue every two years until you have repaid the Shared Equity Amount in full.

Disclaimer

The above FAQs are indicative and provide general information around the operation of the Boost to Buy Home Ownership Scheme in relation to certain property scenarios and should not be relied upon nor treated as a sole source of information. The FAQs do not consider your individual objectives, financial situation or needs. Before basing any decisions on this information please:

- consider if it is appropriate to your circumstances; and

- consider obtaining advice specific to your needs including financial, taxation and legal advice.

Scheme applications are subject to Queensland Government approval. Loan applications to the approved lender are subject to credit approval with any loan offer including full terms and conditions. The information contained within in this document is provided in good faith in relation to the information available at the time of its preparation and is subject to change.